The 2019 Q3 biotech and pharmaceutical transactions were defined by an active M&A market as deal value increased across all categories when compared to the same period in 2018 (source: Medtrack Informa Database). Licensing deals remained flat when compared to the same period last year.

M&A and Licensing Season

The bio-tech market experienced fewer deals in Q3 2019 relative to Q3 2018, but deal value was higher at $62.0 billion in Q3 2019 compared to $37.3 billion in Q3 2018. The market was mostly driven by larger licensing agreement deals and M&A deal activity. Q3 2019 includes Skyhawk Therapeutics’ $2.0 billion licensing agreement with Genentech. The two counterparts will partner to discover and develop small molecule RNA splicing modifiers for oncology and neurodegenerative diseases.

Q3 2019 deal volume in the M&A market is up by 36% year over year reaching $20.2 billion for the quarter. Most notably, Celgene announced its $13.4 billion acquisition of Amgen as the story of mega deals continued into Q3 2019. Permira Funds also announced its acquisition of Cambrex, a small molecule company providing drug substance, drug product and drug analytical services across the entire drug lifecycle, for $2.4 billion. And finally, Swiss pharmaceutical giant Novartis announced that it will be acquiring Vertex Pharmaceuticals for $950 million. The Vertex acquisition is Novartis’s third large acquisition in 2019.

The number of public offerings increased to 49 in Q3 2019, up from 31 offerings during the same period last year. The offerings include Morphic Holding (a Teknos client), which raised gross proceeds of approximately $90 million in the quarter. That said, IPO activity overall has dampened significantly compared to the Q2 2019 IPO market.

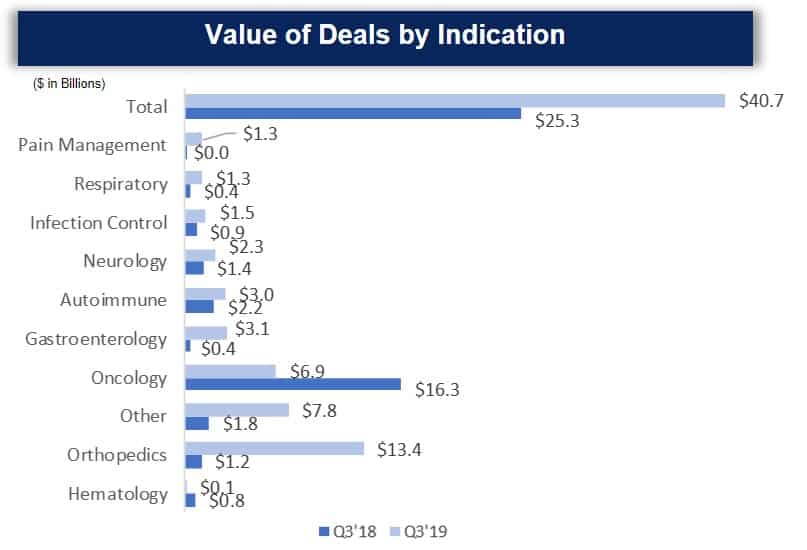

Orthopedics and Oncology Deals On Top

Driven by Celgene’s acquisition of Amgen, orthopedics related companies topped the rest of the pack in terms of deal size, totaling $13.4 billion. However, deal volume involving orthopedics related companies decreased by 55% in Q3 2019 in comparison to the same period last year. The orthopedics segment is expected to see continued large deal activity as Stryker recently announced its acquisition of Wright Medical, at a proposed $4 billion valuation.

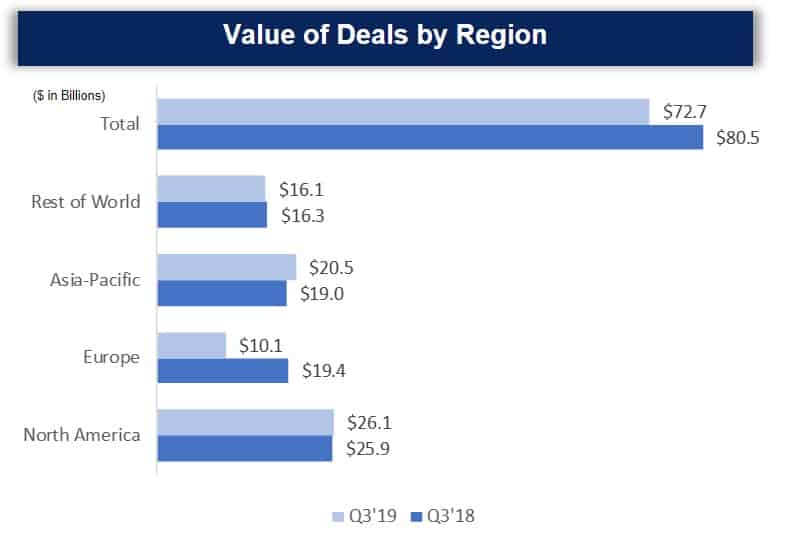

North America Continues to Lead in Number of Deals

Overall, total deal value and number of deals were down from $80.5 billion and 598 deals in Q3 2018 to $72.7 billion and 380 deals in Q3 2019.

North America more than triples Europe in deal volume with 184 announced deals in comparison to 59 deals announced in Europe, as well as more than doubling total deal size in Europe which totaled $10.1 billion in comparison to $26.1 billion in North America. Deal volume declined by 50.1% and 57.8% in the North American and European regions in comparison to Q3 2018. Asia-Pacific region decreased by 4% in Q3 2019 in terms of deal volume with total deal value reaching $20.5 billion, slightly up from $19.0 billion in the same period last year.

How can we help?

Trying to make sense of these issues requires a deep understanding of the biotechnology market, as well significant knowledge of how biotechnology companies operate. Teknos Associates is uniquely positioned as a result of our significant experience working closely with biotechnology companies at all stages of development. We have assisted organizations with valuations associated with future sales, examined the potential value of therapies to help guide companies in the allocation of their research and development efforts, and performed strategic analyses to assist in positioning companies for organic and inorganic growth.

To learn more, please view our presentation and contact us at info@teknosassociates.com .

Note: Transaction totals may not sum across different types, indication, and regions due to available data.

Biotech and Life Sciences: Q3 2019 Summary

The 2019 Q3 biotech and pharmaceutical transactions were defined by an active M&A market as deal value increased across all categories when compared to the same period in 2018 (source: Medtrack Informa Database). Licensing deals remained flat when compared to the same period last year.

M&A and Licensing Season

The bio-tech market experienced fewer deals in Q3 2019 relative to Q3 2018, but deal value was higher at $62.0 billion in Q3 2019 compared to $37.3 billion in Q3 2018. The market was mostly driven by larger licensing agreement deals and M&A deal activity. Q3 2019 includes Skyhawk Therapeutics’ $2.0 billion licensing agreement with Genentech. The two counterparts will partner to discover and develop small molecule RNA splicing modifiers for oncology and neurodegenerative diseases.

Q3 2019 deal volume in the M&A market is up by 36% year over year reaching $20.2 billion for the quarter. Most notably, Celgene announced its $13.4 billion acquisition of Amgen as the story of mega deals continued into Q3 2019. Permira Funds also announced its acquisition of Cambrex, a small molecule company providing drug substance, drug product and drug analytical services across the entire drug lifecycle, for $2.4 billion. And finally, Swiss pharmaceutical giant Novartis announced that it will be acquiring Vertex Pharmaceuticals for $950 million. The Vertex acquisition is Novartis’s third large acquisition in 2019.

The number of public offerings increased to 49 in Q3 2019, up from 31 offerings during the same period last year. The offerings include Morphic Holding (a Teknos client), which raised gross proceeds of approximately $90 million in the quarter. That said, IPO activity overall has dampened significantly compared to the Q2 2019 IPO market.

Orthopedics and Oncology Deals On Top

Driven by Celgene’s acquisition of Amgen, orthopedics related companies topped the rest of the pack in terms of deal size, totaling $13.4 billion. However, deal volume involving orthopedics related companies decreased by 55% in Q3 2019 in comparison to the same period last year. The orthopedics segment is expected to see continued large deal activity as Stryker recently announced its acquisition of Wright Medical, at a proposed $4 billion valuation.

North America Continues to Lead in Number of Deals

Overall, total deal value and number of deals were down from $80.5 billion and 598 deals in Q3 2018 to $72.7 billion and 380 deals in Q3 2019.

North America more than triples Europe in deal volume with 184 announced deals in comparison to 59 deals announced in Europe, as well as more than doubling total deal size in Europe which totaled $10.1 billion in comparison to $26.1 billion in North America. Deal volume declined by 50.1% and 57.8% in the North American and European regions in comparison to Q3 2018. Asia-Pacific region decreased by 4% in Q3 2019 in terms of deal volume with total deal value reaching $20.5 billion, slightly up from $19.0 billion in the same period last year.

How can we help?

Trying to make sense of these issues requires a deep understanding of the biotechnology market, as well significant knowledge of how biotechnology companies operate. Teknos Associates is uniquely positioned as a result of our significant experience working closely with biotechnology companies at all stages of development.

To learn more, please view our presentation and contact us at info@teknosassociates.com .

Note: Transaction totals may not sum across different types, indication, and regions due to available data.