Background

Internal Revenue Code section 1202 (IRC 1202) – Qualified Small Business Stock, allows capital gains from select small business stock to be excluded from federal tax. The code was designed to provide an incentive for non-corporate taxpayers to invest in small businesses. The code has a few interesting characteristics:

- IRC 1202 applies to “qualified small business stock” (QSBS) acquired after September 27, 2010 that has been held for more than five years.

- The statute provides an exclusion from income for any gain from the sale or exchange of QSBS. The gain exclusion percentages apply to QSBS issued during very specific time periods:

- 50% for QSBS issued before February 18, 2009.

- 75% for QSBS issued between February 18, 2009 and September 27, 2010.

- 100% for QSBS issued after September 27, 2010.

Only the stock of C corporations (or partnerships electing to be taxed as a C corporation) can qualify for QSBS. Many businesses have historically ignored planning for QSBS due to high corporate tax rates and the imposition of double taxation (i.e., income taxes at both the corporate and shareholder levels). However, the reduction of the corporate tax rate from 35% to 21% (2017 Tax Cuts and Jobs Act) has turned the tables, creating an ideal time for private companies and their investors to review the fundamentals of QSBS treatment and the particulars of IRC 1202. In addition, the capital gains that are exempt from tax under this section are also exempt from the 3.8% net investment income (NII) tax applied to most investment income.

Analysis and Recommendations

The management of an established technology hardware company and their tax advisors contacted Teknos to discuss their valuation needs relative to IRC 1202. In 2014, the company filed form 8832 electing to be an LLC taxed as a C corporation. Due to their check-the-box election, the gain exclusion percentages (50%, 75%, 100%) are dependent on the values assigned to the assets with holding periods that fall into the three date ranges noted in the above paragraph. The company was acquired by another entity in 2018 for approximately $200 million.

Teknos provided two valuation reports as of January 2014, opining on (i) the fair market value of the company’s total assets, and (ii) the fair market values of the company’s applicable identifiable assets, allocated into the three holding period groups. The resulting total asset value at 2014 was approximately $25.0 million. The criteria listed below must be met in order for all of the gain to be eligible for an exclusion (to note, these criteria have been oversimplified for these purposes and there are additional nuances to be considered). The company’s valuation of total assets meets all three criteria, allowing all of the gain to be eligible for an exclusion.

- Each taxpayer (investor) is entitled to exclude up to the greater of $10 million gain or 10x their investment. The valuation implies an investment of $25 million (IRS views the check-the-box 8832 election as a change in control). The estimated gain of $175 million (2018 sale for approximately $200 million less starting basis of $25 million) is less than 10x the investment (10 x $25 million = $250 million).

- The value of the assets contributed ($25 million) cannot exceed $50 million at the measurement date or any earlier period.

- More than 80% of the valued assets must represent business assets (as opposed to investment assets).

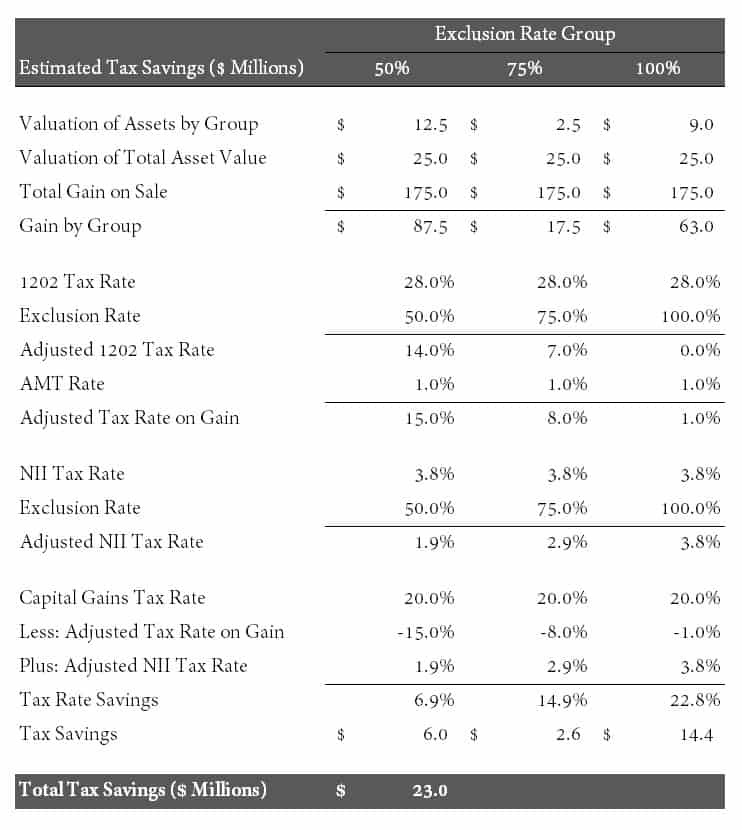

The valuation covering the fair market value of the company’s identifiable assets allows for a calculation of the gain exclusions and tax savings by holding period group under IRC 1202. The identified assets included fixed assets, customer relationships, developed technology, patents, trademarks, and assembled workforce. Approximately $3.5 million, $2.5 million, and $9.0 million were allocated to the applicable identified asset holding period groups representing gain exclusion percentages of 50%, 75%, and 100%, respectively. Goodwill of $9.0 million was also added to the 50% gain exclusion group for a total of $12.5 million. The estimated tax savings are calculated in the table below (to note, these calculations are oversimplified and are for illustrative purposes only):

Results

Teknos presented the two valuations to the company’s management, which confirmed that their investors both qualified for the gain exclusions and provided a basis for estimating their overall tax savings. Per the calculations above, the tax savings for the company’s investors are estimated at $23.0 million (on a $200 million sale of the business) by qualifying for IRC 1202.

Teknos Associates provides valuation and advisory services for emerging growth companies and their venture capital backers. Clients rely on our financial expertise, knowledge of technology markets, and high standards to deliver relevant and timely valuation reports and fairness opinions.

Special Note: From time to time, Teknos Associates has been retained by the Internal Revenue Service to perform valuation services. However, nothing in this communication may be taken to represent the official position or policy of the IRS. The opinions expressed herein are those only of Teknos Associates.

IRS Circular 230 Disclaimer: Pursuant to regulations governing the practice of attorneys, certified public accountants, enrolled agents, enrolled actuaries, and appraisers before the Internal Revenue Service, unless otherwise expressly stated, any U.S. federal or state tax advice in this communication (including attachments) is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of (i) avoiding penalties that may be imposed under federal or state law or (ii) promoting, marketing, or recommending to another party any transaction or tax-related matter(s) addressed herein.